Your Guide to Therapy Eligibility: Requirements Explained

- tjdontplay

- 8 hours ago

- 8 min read

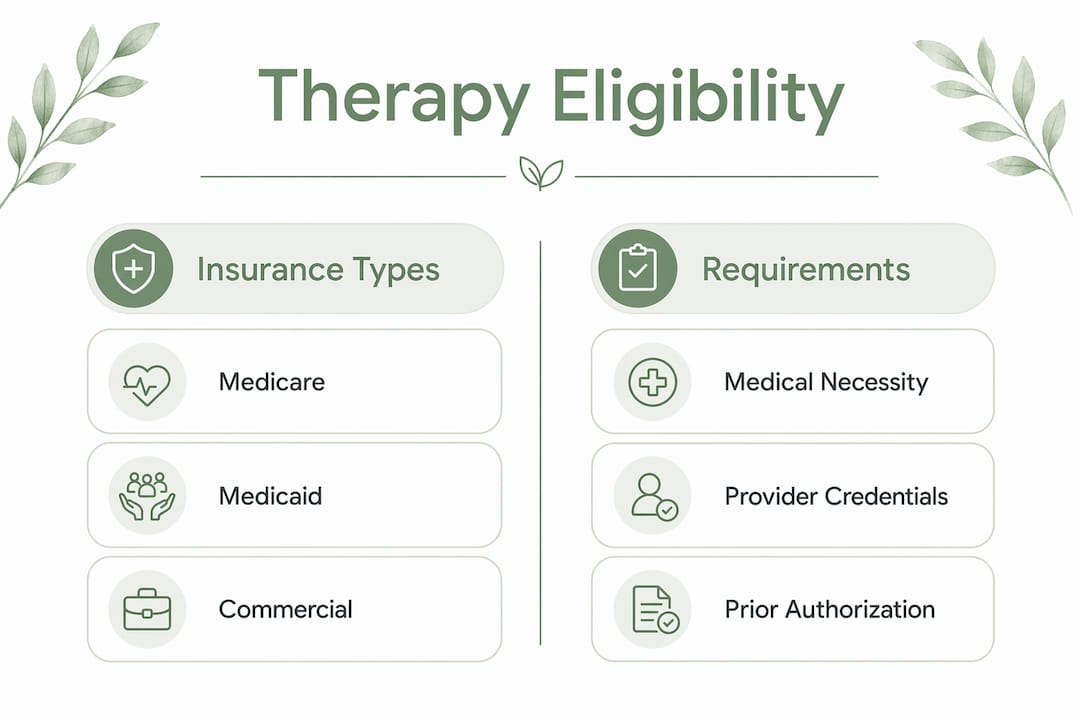

Therapy eligibility is defined by three factors: medical necessity, insurance plan rules, and provider credentials. Together, these determine whether your physical or craniosacral therapy sessions are covered and how many you can access. This guide to therapy eligibility walks you through each factor clearly, so you can approach your coverage with confidence. Whether you hold Medicare, Aetna, Cigna, Emblem, or United Healthcare, the rules follow a consistent framework once you understand the core terms. Knowing what qualifies you for therapy is the first step toward getting the care you need.

What is the guide to therapy eligibility based on?

Therapy eligibility criteria rest on one central concept: medical necessity. Insurance companies define medical necessity as the requirement that therapy treat a documented, diagnosed condition rather than support general wellness. A DSM-5-TR diagnosis is required for coverage, meaning your therapist or referring physician must link your treatment to a specific clinical condition.

This distinction matters more than most patients realize. Life coaching, stress management without a clinical diagnosis, and relationship enrichment programs do not qualify as medically necessary under most insurance plans. Insurance treats covered therapy as medical care, not personal development.

For physical therapy, medical necessity typically means a documented musculoskeletal injury, post-surgical recovery need, or chronic pain condition. For craniosacral therapy, the bar is similar: a licensed provider must document a clinical rationale tied to a recognized diagnosis. Without that documentation, your insurer has grounds to deny the claim.

Pro Tip: Ask your provider to give you a copy of the clinical notes submitted to your insurer. Reviewing this documentation helps you catch errors before a denial occurs.

Here is what medical necessity documentation typically includes:

A formal diagnosis using ICD-10 codes

A description of how the condition limits your daily function

A treatment plan with measurable goals and a projected timeline

Progress notes showing improvement or continued clinical need

A physician referral or prescription where required by your plan

Session limits are also tied to medical necessity. Insurers approve a set number of sessions upfront and require updated documentation to authorize more. Staying on top of this paperwork prevents unexpected gaps in your care.

How do insurance types affect therapy eligibility requirements?

Your insurance plan type shapes your therapy eligibility requirements more than almost any other factor. Medicare, Medicaid, PPO, and HMO plans each impose different rules on referrals, copays, and prior authorization.

Medicare Part B covers outpatient therapy when medically necessary. For 2026, Medicare Part B applies a 20% coinsurance after a $283 deductible. That means once you meet the deductible, you pay one-fifth of each approved session cost. Contemporaryrehabservices accepts Medicare, which removes a significant barrier for patients in Nassau County and Queens.

Medicaid coverage varies by state. In expansion states, Medicaid covers adults up to 138% of the federal poverty level. Prior authorization is typically required after 8–12 sessions, meaning your provider must submit additional clinical justification to continue treatment. Failing to request that authorization on time can result in denied claims even when your condition clearly warrants continued care.

The table below shows how plan types compare on key eligibility factors:

Plan type | Referral required | Typical copay | Prior authorization |

Medicare Part B | Sometimes | 20% after $283 deductible | Yes, for extended care |

Medicaid | Varies by state | Low or none | Yes, after 8–12 sessions |

PPO | No | $20–$50 per session | Sometimes |

HMO | Yes | $20–$50 per session | Often required |

Under the Mental Health Parity and Addiction Equity Act (MHPAEA), insurance plans must cover therapy at rates comparable to specialist medical visits. Copays typically fall between $20 and $50, with coinsurance ranging from 20% to 40%. If your plan covers a cardiologist visit at a $30 copay, it cannot charge you $75 for a therapy session.

Pro Tip: Call the member services number on your insurance card before your first appointment. Ask specifically about your outpatient therapy benefit, your deductible status, and whether prior authorization is needed.

In-network providers cost significantly less than out-of-network providers. Choosing a clinic like Contemporaryrehabservices that is already credentialed with your insurer removes the need to navigate out-of-network reimbursement entirely.

How do you check your eligibility for physical or craniosacral therapy?

Checking your therapy eligibility requirements takes a few deliberate steps. Skipping any one of them is where most patients run into billing surprises.

Call your insurance plan. Ask for your outpatient therapy benefit details. Confirm your deductible, copay or coinsurance amount, session limits, and whether prior authorization is required before your first visit.

Verify provider network status. Confirm that your therapist is in-network with your plan. A provider directory on your insurer’s website is a starting point, but always call the clinic directly to confirm current network participation. Directories are not always updated in real time.

Check credential requirements. Physical therapists must hold a state license. Craniosacral therapy credentials vary. Look for practitioners trained through recognized programs and verify their standing with your state’s licensing board. A holistic practice credentials guide can help you understand what certifications carry clinical weight.

Confirm referral requirements. HMO plans generally require a primary care physician referral before you can see a specialist. PPO plans and self-pay arrangements typically allow direct access without a referral. Knowing this in advance saves you a wasted appointment.

Gather your documentation. Your provider needs a diagnosis, a treatment plan, and progress notes to justify ongoing sessions. Ask your referring physician for a written prescription or referral letter that includes your diagnosis code.

Understand your self-pay option. If your insurance does not cover a specific therapy type, self-pay rates are often negotiable. Paying out of pocket also gives you more privacy, since insurance coverage requires a formal diagnosis that becomes part of your medical record.

For a detailed walkthrough specific to physical therapy, the PT eligibility guide at Contemporaryrehabservices covers each step with plan-specific examples.

What are the most common mistakes when verifying therapy eligibility?

Most eligibility problems are preventable. They stem from assumptions patients make before confirming the details with their insurer or provider.

Assuming a referral is always required. Many patients delay starting therapy because they believe they need a physician referral first. PPO plans and self-pay arrangements allow direct access. Only HMO plans consistently require a referral as a condition of coverage.

Not confirming network status in advance. A therapist listed in your insurer’s online directory may have changed network status. Always call the clinic and your insurer to confirm before your first session.

Missing prior authorization deadlines. Medicaid and some commercial plans require authorization before therapy begins or before extending sessions beyond the initial approved number. Missing this window can result in denied claims for sessions you already attended.

Assuming all therapy modalities are covered equally. Physical therapy has well-established insurance billing codes. Craniosacral therapy billing varies by insurer and may require additional documentation of clinical necessity. Verify coverage for the specific modality before booking.

Not knowing how superbills work. If you see an out-of-network provider, you can request a superbill for reimbursement. A superbill is an itemized receipt containing CPT codes and diagnosis codes that you submit directly to your insurer. Out-of-network reimbursement requires meeting a separate, usually higher, deductible first.

“Session limits under mental health parity laws must be comparable to medical visit limits, but enforcement can be inconsistent. Prior authorizations help extend coverage when clinical justification is documented clearly.” — Insurance coverage guidance, 2026

When your insurer denies a claim, you have the right to appeal. Request the denial reason in writing, ask your provider to submit additional clinical notes, and file a formal appeal within the deadline stated in your denial letter. Most successful appeals include updated progress notes that directly address the insurer’s stated reason for denial.

Key Takeaways

Therapy eligibility is determined by medical necessity, insurance plan type, and provider credentials working together, not by any single factor alone.

Point | Details |

Medical necessity is required | Insurance covers therapy only when tied to a documented clinical diagnosis, not general wellness. |

Plan type shapes your costs | Medicare, Medicaid, PPO, and HMO plans each carry different copays, referral rules, and session limits. |

Verify before your first visit | Confirm network status, prior authorization needs, and deductible status before booking any session. |

Superbills enable out-of-network claims | Out-of-network patients can submit itemized superbills for reimbursement after meeting a separate deductible. |

Referrals are not always required | PPO plans and self-pay arrangements allow direct access to therapy without a physician referral. |

What I’ve learned about therapy eligibility after years of working with patients

The most consistent pattern I see is that patients who struggle to access therapy are not struggling because of their diagnosis or their insurance plan. They are struggling because they did not ask the right questions before their first appointment.

Insurance paperwork feels like a barrier, but it is mostly a checklist. Medical necessity documentation, prior authorization, referral requirements: each one has a clear answer if you ask directly. The patients who get the most out of their coverage are the ones who treat the initial conversation with their insurer and their provider as a two-way exchange, not a formality. Treating that first consultation as an interview where you evaluate the provider’s credentials and communication style leads to better outcomes.

There is one thing most guides skip: the privacy dimension. When insurance covers your therapy, your diagnosis codes become part of your record and may be accessible to future disability insurers. That is not a reason to avoid insurance coverage. It is a reason to understand what you are agreeing to. For some patients, self-pay is worth the cost specifically because it keeps their records private. That is a legitimate choice, and a good provider will explain it to you without judgment.

The practical takeaway: call your insurer before your first session, confirm your provider’s network status directly, and ask your therapist what documentation they submit on your behalf. Those three steps resolve the majority of eligibility problems before they start.

— Tj

Physical and craniosacral therapy at Contemporaryrehabservices

Contemporaryrehabservices is a boutique physical therapy clinic in Albertson, NY, serving patients across Nassau County and Queens. The clinic accepts Medicare, Aetna, Cigna, Emblem, and United Healthcare plans, which covers the majority of patients in the area.

The team at Contemporaryrehabservices helps patients verify their therapy eligibility and understand their insurance benefits before their first visit. Locations in Albertson, Herricks, Roslyn, and East Williston make access straightforward across Long Island. Physical therapy and craniosacral therapy services are tailored to meet the documentation and credentialing standards your insurer requires. To confirm your coverage and book a consultation, visit Contemporaryrehabservices directly.

FAQ

What does “medically necessary” mean for therapy coverage?

Medically necessary therapy is treatment tied to a documented clinical diagnosis using ICD-10 or DSM-5-TR codes. Insurance covers therapy as medical care, not personal development or wellness coaching.

Do I need a referral to start physical therapy?

PPO plans and self-pay arrangements generally allow direct access without a referral. HMO plans typically require a primary care physician referral before covering specialist or therapy visits.

How many therapy sessions does insurance cover?

Session limits vary by plan. Medicare and most commercial plans approve an initial set of sessions and require updated clinical documentation to authorize more. Medicaid often requires prior authorization after 8–12 sessions depending on the state.

Is craniosacral therapy covered by insurance?

Coverage for craniosacral therapy depends on your specific plan and the provider’s credentials. Some insurers cover it under physical therapy billing codes when medical necessity is documented. Verify with your insurer before booking.

What is a superbill and when do I need one?

A superbill is an itemized receipt with CPT and diagnosis codes that you submit to your insurer for out-of-network reimbursement. You typically need to meet a separate out-of-network deductible before reimbursement applies.

Recommended

Comments